The U.S. dollar’s performance in 2025 has been strange. I don’t say this only because the dollar has fallen by about 10% since the beginning of the year. I say it because the relationships between the dollar and long-term Treasury yields, and between the dollar and U.S. equities, look very different from what we’ve seen through most of history.

US - Dollar Index

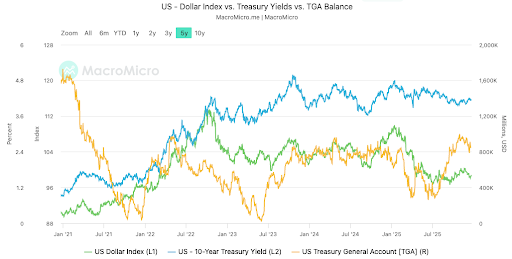

For most historical periods, the dollar and long-term Treasury yields have been positively correlated. The logic is simple: higher yields attract foreign capital into safe U.S. assets, increasing demand for dollars. But in 2025, as the chart below shows, the 10-year Treasury yield (the blue line) has stayed high, while the dollar (the green line) has steadily weakened.

US - Dollar Index vs. 10Y Treasury Yield

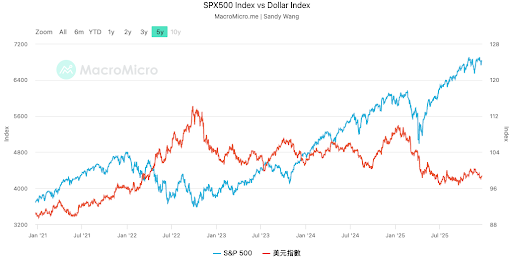

The same kind of divergence has appeared between the dollar and the S&P 500. Historically, the dollar and U.S. equities have usually moved in the same direction. Since April this year, however, that relationship has broken down.

So what’s behind this?

You can probably guess the answer. Aggressive tariff policies, the so-called “big and beautiful” fiscal legislation, and excessive interference with the Federal Reserve—which raises doubts about its independence—have all contributed to growing concerns about U.S. sovereign credit. People are starting to ask uncomfortable questions: Can U.S. debt really be brought under control? Can the government continue to service it? Will inflation eventually spiral out of control?

Howard Marks, Jeffrey Gundlach, and other investors have expressed similar concerns.

In one memo, The Calculus of Value (August 13, 2025), Howard Marks wrote: “The U.S. fiscal deficits and national debt show no sign of improvement, and worldwide concern over them seems to be increasing.” In another memo, More on Repealing the Laws of Economics (June 18, 2025), he said: “We’re simply not tackling our deficits. We’re not implementing meaningful spending cuts or tax increases.” “No one can say when, but it makes sense to assume we’ll eventually reach a point at which our credit is no longer unlimited and our interest rates are no longer so low.”

Jeffrey Gundlach (https://www.youtube.com/watch?v=n7JV_DaBFXk) has raised related issues, especially around the financing of long-term Treasuries. The U.S. is issuing a large volume of debt, while fiscal and monetary policies remain inflationary. What’s unusual is that although the Federal Reserve has been cutting rates for more than a year, long-term Treasury yields are now higher than they were before those cuts. This has never really happened before.

Over the past 12 months, about 80% of newly issued Treasuries have maturities of less than one year. Only around 1.7% have maturities of 20 to 30 years. Why? The reason is similar to why people rely on credit cards: short-term borrowing is cheaper, easier, and immediately available. But it also plants the seeds of a much bigger problem down the road.

Right now, the U.S. fiscal deficit is about 6% of GDP—a level that usually appears only during crises or emergencies. And this is happening while the economy itself isn’t in obvious trouble. All it would take is a recession for the deficit to widen further, likely jumping to 10% or even 14% of GDP.

What happens then? The system could start to tear. Roughly 30% of U.S. government tax revenue already goes toward paying interest on the national debt. If current trends continue, by around 2030 more than half of government revenue—close to 60%—could be consumed by interest payments alone. In a worse scenario, total tax revenue might not even be enough to cover interest, pushing the system into a Ponzi-like dynamic: borrowing new money just to pay interest on old debt.

As Warren Buffett said at the May 3 Berkshire Hathaway annual meeting: “We’re operating at a fiscal deficit now that is unsustainably over a very long period of time. We don’t know whether this means two years or 20 years, because there’s never been a country like the United States. But this is something that can’t go on forever…and it gets uncontrollable at a certain point.”

Against this backdrop, investors have begun to reduce their exposure to dollar risk. One way they do this is by selling long-term U.S. Treasuries, which helps explain why long-term yields have risen instead of fallen.

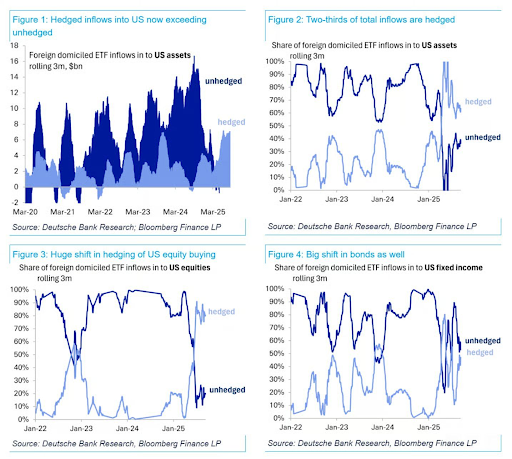

At the same time, investors still have confidence in U.S. companies. They are willing to invest in U.S. equities, but they increasingly hedge their dollar exposure. As the chart below (Figure 3) indicates, where roughly 80% of foreign investment used to be unhedged, now around 80% is hedged. In effect, investors are trying to separate confidence in U.S. corporations from concerns about U.S. sovereign credit.

This helps explain why, over the past year, the dollar has diverged from both long-term Treasury yields and the stock market. It also helps explain why asset prices in other parts of the world have surged in 2025. Take gold, for example: it’s up about 60% year to date, even though its long-term annualized return from December 1978 to November 2025 is only around 6.8%.

Jeffrey Gundlach’s suggested asset allocation reflects this view: a maximum of 40% in equities (primarily non-U.S.), 25% in fixed income (including non-dollar and emerging market debt), 15% in gold, and the rest in cash.

That implies virtually no exposure to the U.S.

What do you think?